Login

Login Sign Up

Sign UpInsurance

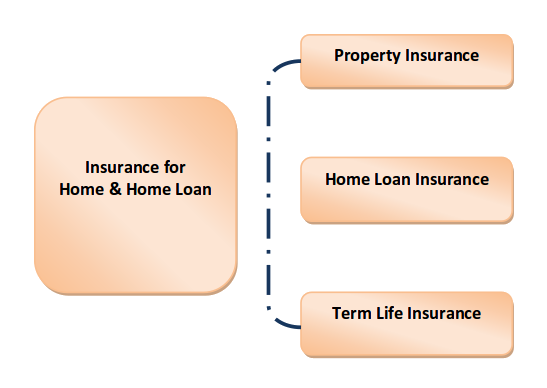

Insurance needs arising out of a home and home loan

Let’s look at each one of them in detail

1) Property Insurance

Scope: Covers damage to the property on account of fire & other natural disasters like earthquake, lightening, floods etc.

Key Features:

a) The one-time premium can be added to the loan amount or paid separately depending on the bank and their general insurance partners.

b) Some banks mandate it and some do not.

c) Cost depends on the size of the property.

d) Tenure will generally be same as that of the home loan. Some banks are fine with a lower tenure.

The Bottomline: If Mr. Mukesh Ambani’s house, Antilia, can catch fire, any other house in India can and therefore the potential damage has to be insured for. Should we say anything more?

2) Home Loan Insurance

Scope: Covers the outstanding home loan amount in case of a premature loss of life of applicant/s.

Key Features:

a) It is a life insurance product & not general insurance.

b) The one-time premium can be added to the loan amount or paid separately depending on the bank and their life insurance partners.

c) It is not mandatory although banks will try to sell this.

Limitation:

a) Coverage is restricted to outstanding loan amount. Suppose you close a 20 year loan in 8 years’ time the insurance coverage ceases to exist.

b) The cost of a Home Loan Insurance Policy is comparatively higher than a Term Insurance Policy of an equivalent coverage amount & tenure.

The Bottomline: A better option would be a term life insurance which eliminates the above limitations.

3) Term Life Insurance

Scope: Covers a “well-thought-out amount” for a “well-thought-out tenure” in case of premature loss of life of applicant/s.

Key Features

a) Well Thought-out Coverage Amount & Tenure – It’s generally 10 times your current annual package plus all outstanding loan amounts that you have or intend to take in the near future and covered for a tenure of atleast your remaining work life.

b) Keep it separate from the home loan and service the premiums (one time or annual) separately.

c) Irrespective of how soon you close the home loan the full coverage will continue for the entire tenure.

d) It is not mandatory for availing a home loan, but it is absolutely necessary for your family’s financial safety.

The Bottomline: Life is uncertain. Should we say anything more?

4) Selection of Term Life Insurance

The legendary Warren Buffet in his annual letter of 2002 mentioned the following regarding Reinsurance Business.

“Cheap reinsurance is a fool's bargain: When an insurer lays out money today in exchange for a reinsurer's promise to pay a decade or two later, it's dangerous - and possibly life threatening - for the insurer to deal with any but the strongest reinsurer around.”

Without paying any royalty to the poor man, we at loangebra, have done a bit of tinkering to his statement in the context of Term Insurance.

“Cheap Term Insurance is a fool's bargain: When you lay out money today in exchange for an insurer's promise to pay a decade or two later, it's dangerous - and possibly sustenance threatening for your family - for you to deal with any but the strongest and safest insurer around.”

The Bottomline: Choose wisely. Remember, the benefit of this product can never be seen during your lifetime. After you, the family should get the benefits without running from pillar to post.